Posted: September 30th, 2010 | Author: OSS Team | Filed under: Around the World | Tags: Analysys Mason, customer experience, LTE, OSS, policy control | Comments Off on Around the World

FierceTelecom…

Putting Policy Control to Work

Editor-in-chief Sue Marek explains the current trend of policy control, as operators shift their business models and start implementing tiered price plans to keep revenue and bandwidth aligned. Although policy control tools are available, some industry experts believe that policy control is an afterthought for operators, and that we may not see a more sophisticated use of the OSS solution until carriers deploy LTE networks. Sue believes tiered pricing packages will probably be the mainstay for awhile, but eventually we will see “policy control 2.0 techniques”, which include real-time transactions and the ability to activate or de-activate new services on the fly. Whatever the implementation, policy control tools will certainly continue to be a hot topic of discussion in the coming months and possibly years ahead, as more operators migrate from 3G to 4G.

European Communications…

Telecoms Bounces Back in 2010

Anne Morris reports on two recent studies from Ovum and Analysys Mason that indicates improved growth for the telecoms service sector in 2010. Some of the reports key highlights include:

- The worldwide telecoms market is poised to resume higher growth rates following the difficulties created by the economic slowdown—principal analyst, Roz Roseboro forecasts that worldwide telecoms revenue will grow at a CAGR of 6% between 2009 and 2014. – Analysys Mason

- John Lively, chief forecaster shares a similar assessment: In 2010, China and India alone will add 329 million new mobile phone connections. This is equivalent to more than the combined total population of Germany, France, Italy, Spain and the UK. – Ovum

- Fixed-line services will continue to decline, although fiber connections for broadband services will increasingly be important for telcos. Overall, the number of fixed lines worldwide will fall from 1 billion in 2010, to 871 million by 2014. Fixed-line services revenues will also fall from around $350 billion to $283 billion, for the same period. – Ovum

- Mobile phone connections will increase from 5.3 billion in 2010 to 7.1 billion in 2014, with the emerging markets of Asia and Africa contributing much of the growth. Revenues from mobile phone services will increase by nearly $100 billion in the three years to 2012. – Ovum

Given these reports and the significant growth CSPs are expected to experience, it will be critical to support data traffic, while recognizing customer’s needs. Operators need to realize that the traditional way to influence customer behavior—through pricing plan and charging options—is not sufficient enough in today’s dynamically changing market.

Mobile Europe…

Mobile Broadband, Content and Data Services Are Key to Helping Operators Combat Falling Retail Revenue, Says Report

According to a recent Analysys Mason study, retail telecoms revenue in Western Europe will continue to decrease by five percent between 2010 and 2015; however, operators can strengthen their positions by concentrating on two main growth areas: mobile broadband and data services. The widespread adoption of flat-rate pricing models has led consumers to expect that their bills will not increase, and created a climate in which it is increasingly difficult for operators to derive more value from new services than they lose from legacy ones. Yanli Suo-Saunders, senior analyst and leader of Analysys Mason’s mobile broadband research programme, states that the “demand for these services will grow as a result of increased service adoption and usage, as content and handset functionality improve. Tiered pricing structures will enable operators to monetize their higher-end smartphone users while also encouraging entry-level service adoption.” The report indicates that a few important new revenue streams have yet to appear, but customer loyalty and trust—and the use of vastly more customer data—will be at the center of those that do emerge.

Posted: September 23rd, 2010 | Author: Special Contributor | Filed under: Telecom Trends | Tags: policy, provisioning, service, telecom | 2 Comments »

By: Dan Baker, Research Director, Technology Research Institute

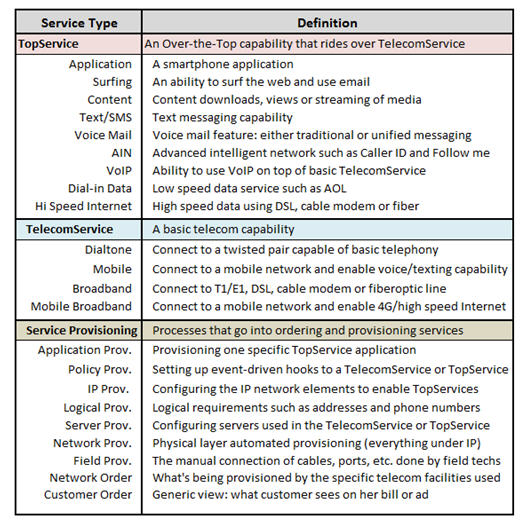

Language—no matter which one—is imprecise in the way that it’s used to explain complex telecom subjects.

A perfect example in English is the term “service”. What exactly does the word mean in a telecom context? I’d guess there are probably 50 unique uses for the word “services” in telecom. Unfortunately, “service” is about as descriptive a word as “thing”.

And as new, over-the-top services emerge, the vocabulary used to describe the “service provisioning” area has also become quite muddy.

Well, here’s my attempt to decipher the terms “service” and “service provisioning” more precisely:

One of the more confusing aspects of service provisioning is the policy area that Comptel is championing. What’s interesting about policy is that while it’s enabled on the telecom side, the policy may actually be implemented and controlled in real time by the over-the-top provider.

You can be sure that in the years ahead our current definitions of what a telecom service is will be stretched dramatically as they were during the last decade.

While I’m sure my table of service terms has some flaws, perhaps you can use these definitions to spark some fruitful discussions with your peers and vendors, or here on “The Dynamics of OSS”.

In the end, I hope my definitions of telecom “service” will be of service to you :- )

Dan Baker is the research director of Technology Research Institute (TRI). Since 1994, Baker has authored dozens of research studies in the BSS/OSS market. He contributes articles to Vanilla Plus and writes a regular column for Billing & OSS World called Dan Baker Blog.

Posted: September 20th, 2010 | Author: Olivier Suard | Filed under: Events | Tags: Comptel User Group, GSMA, Management World, Mobile World Congress, TM Forum | 1 Comment »

Moving home is consistently rated amongst the most stressful things in life (up there with divorce and bereavement). It’s no wonder really. Aside from all of the logistics involved, there are many emotional attachments associated with the old home—the happy memories, the neighbours, the favourite shops and restaurants… it’s so hard leaving all of those things behind.

In recent weeks, both the GSMA and TM Forum have announced plans to move their flagship events—Mobile World Congress (MWC) and Management World (still known in most circles as TMW), respectively. Admittedly, the GSMA have not actually announced they are moving, but for the 2013 event and onwards, they are considering six alternative cities, including Barcelona, the present home of the MWC. At least their customers (operators, press, exhibitors and sponsors) are given a chance to express their preferences rather than waiting to be presented with a fait-accompli.

As a prospective delegate and exhibitor, one can’t help feeling a little unsettled about the prospect of moving. One needs to get used to new exhibition layouts (where are the best spots?), new hotels (will we find a nice, affordable place?), new restaurants and bars (for those all important, post-event meetings) and even a new climate (TMW’s new home, Dublin, is not Nice, as Ray Le Maistre of Light Reading pointed out)… There is also the uncertainty of whether the show will attract the same level and quality of participation, and whether as a sponsor, one should invest at the same level as in past events.

That said, one has to feel some sympathy for the organizers—moving an event is not a simple decision or operation. Every year, Comptel organizes the Comptel User Group (CUG) in a different country, so we know first hand how fraught with difficulty choosing a venue can be (can delegates fly there cost effectively?, will they need visas?, will it coincide with some holiday?). And yes, we have made mistakes in the past, but as Oscar Wilde once said: ‘Experience is the name everyone gives to their mistakes.”

Posted: September 17th, 2010 | Author: OSS Team | Filed under: Around the World | Tags: BSS, LTE, OSS, TM Forum | Comments Off on Around the World

Light Reading…

OSS: The Missing Link

In addition to our very own Bob Machin having attended the OSS/BSS World Summit, Light Reading’s Ray Le Maistre reported from the show floor. During the event, Ibrahim Gedeon, CTO of Canadian carrier Telus Corp., discussed Service Provider Information Technology (SPIT)—a Light Reading term for the evolving set of non-traditional telecom technologies—and how OSS/BSS can, when utilized to their true potential, help service providers “monetize their networks”. Gedeon explained that it is the OSS specialists within the carriers who are the key figures in terms of new service creation; this is largely attributed to vendor integration roadblocks. Having identified this a few years ago, Comptel designed a portfolio of OSS solutions to help CSPs adapt to all common telecoms network and IT environments and evolve to meet the demands of future services.

Want to learn more about the SPIT concept? Check out the SPIT Manifesto, which highlights its importance in the telecom infrastructure ecosystem.

GigaOM…

LTE to Boost Demand for Mobile Bandwidth, Network Gear

Om Malik explores the current state of mobile broadband and the excessive data usage employed by consumers in his recent GigaOm blog post. He points out that every time we log on to Facebook or fire up our browsers, we are adding to the pressure on wireless networks and making carriers rethink their plans (e.g. end unlimited data usage plans). He also references several interesting industry reports in his post. One from research firm In-Stat states that mobile carriers are going to spend nearly $117 billion by 2014 (up 41 percent from 2009’s spend of $83 billion) on last mile backhaul (including line leasing, new equipment-spending, and spectrum acquisitions). Om continues to state that wireless last mile backhaul capacity in Western Europe will more than triple between 2010 and 2014, to nearly 60,000 Gbps, and that the pressure on the networks is only going increase with the launch of LTE-based wireless broadband networks.

TM Forum Community…

LTE Is Coming….But Don’t Fall For The Hype!

Contrary to what Om blogs about in the previous highlight, Martin Creaner from TM Forum doesn’t see why we are treating LTE with such urgency. He points out that it has been widely publicized over the last year that there will be 22 operator LTE launches in 2011, but as far as he knows there have been three so far this year. He believes that 3G is really only now delivering its promise—with good stable high data speeds and a wide availability of handsets in multiple global regions. As for Martin’s views on LTE, “when launched [it] will undoubtedly be a data-only service, available in very, very few regions, and with voice-centric handset availability being a couple of years in the future”. He is a great believer in the need for continuous improvement, but tells us not to fall for any hype that tells you 4G is here. Do you agree or disagree with Martin’s views on LTE?

Posted: September 10th, 2010 | Author: Bob Machin | Filed under: Events | Tags: BSS, cloud, customer experience, OSS, policy control, transformation | Comments Off on OSS/BSS World Summit in London, 8-9 September

This week, OSS/BSS World hosted a conference in the Park Lane Hotel, London. I went along for Comptel, and here, pretty much as I wrote them, are my notes from the two days.

Overall Thoughts

Well-attended and heavily-sponsored conference, indicating that OSS and BSS are still hot topics in the industry. Good mix of operators, SIs and many hardware and software vendors. Full agenda (somewhat weighted to the BSS side ) with speakers limited to 20- or 25-minute slots for presentations and questions—an increasingly common (and welcome) approach at conferences. Contributions from the floor seemed to me to be relatively few; after the first three keynote presentations, there had been no questions at all. Perhaps we’re at a stage where everyone understands the big themes and is really looking for solid, proven business cases and answers. I suspect that the audience may have been looking for validation of ideas that are already well-grounded about future developments in the industry; if so, they are not likely to have been disappointed.

Themes

Common themes which prevailed across the two days included:

- Customer experience, and focusing on the key points of customer interaction (referenced by Lois Kraus of AT&T as LB-GUPS, or Learn, Buy, Get, Use, Pay, Service, an acronym which even she didn’t seem very keen on). The frequency of new service rollout is making it harder than ever to keep on top of the customer experience. Customer data (and understanding) was regularly referenced as a key differentiator for telcos and potentially a secondary asset which could be exploited more effectively in relationships with partners. Customer retention strategy was acknowledged as more important than acquisition strategy by Emtel of Mauritius.

- Cloud services: many of the questions which arose were of the ‘what difference will Cloud make to this?’ variety. From the platform, the general take was that Cloud was a different world—with great revenue potential but also putting very different demands on carriers. George Nazi of BT Group (President, 21CN, Global Networks and Computing Infrastructure) believed carriers saw it as their ‘single biggest strategic challenge’ but was bullish about its potential and viability. AT&T, when asked about whether its OSS/BSS platform (developed to be universal for all services) would support Cloud, stated that yes, initially it would be used, but later expressed doubt that that approach would be sustainable and suspected that the Cloud business would eventually need its own support. The idea of using Cloud services to support their own businesses (using remote infrastructure and storage as a service, for example) is already prevalent among new ’agile’ communications players.

- Services environment complexity and how it should be handled. Convergence, transformation and consolidation were regularly referenced, as were issues around legacy IT and services and the challenges of migrating these to new platforms (it seems that some problems will always be with us). ‘Transformation’, in particular, was addressed almost as a desirable end in its own right by several speakers (particularly those with SI interests) although the nature and objectives of any transformation could naturally vary greatly. HP cited consolidation and cost reduction, customer experience improvement and the shift to new business models as common objectives of transformation exercises. At a higher level, ‘transformation’ was positioned as a key enabler of an almost philosophical shift in the business—from ‘technology to business’ (look out for T2B as an emerging acronym) and from ‘survive to thrive’. SDPs continue to be popular as a means to open up the service environment to third-party providers and developers. Telefonica are vigorous proponents of this approach and claim to have reduced service rollout time from 6-12 months to 6-12 weeks (quoted by Capgemini).

- Revenue challenges, particularly arising from the ‘data crunch’. The end of flat-rate charging was regularly cited but with few firm theories about how variable charging would play. Orga recited what is fast becoming the industry mantra on real-time charging and policy control as the twin levers of power.

- Machine-to-machine communications and other plays on connected devices, though with little firm opinion of the impact of this on carriers. This was part of a broader theme, however, that ‘communications services’ weren’t dead, that we would see interesting things emerge in the next few years (from the interconnection of devices, in particular) and that carriers, as masters of networks and conmmunications, had a big part to play in the transformation of society which this would drive. As Paulo Collela of Ericsson opined, CSPs should not resign themselves to just being enablers for new players, but should look for ways to be significant agents of change themselves. On day two, Sanjay Mewada of Netcracker spoke on the value of machine-to-machine communications, valuing this as already a $14 billion business—but significantly, he included handset-to-machine transactions, or mobile payments, in his definition of M2M.

Posted: September 6th, 2010 | Author: Bob Machin | Filed under: Telecom Trends | Tags: customer experience, policy control, QoE, QoS | Comments Off on New Business Models? What New Business Models? Part II

Part Two

In my previous post I discussed some ideas that were stimulated by a UK business news piece on Tune hotels.

The second piece in that bulletin concerned Hamleys, the biggest toyshop in London, and arguably one of the most famous in the world. The CEO was being interviewed about the impact of the recession on the store, which doesn’t discount its items. Wasn’t the recession driving their customers elsewhere, asked the interviewer – to go online, for instance, or to visit “stack-‘em-high, sell-‘em-cheap” out-of-town retailers, like Toys‘R’Us?

No, he replied, that hadn’t been their experience, and nor had they been forced into price wars with low-cost rivals.

What kept people coming to Hamleys, he said, was the unique experience that the store could offer, and the company had focused even harder on that. Rivals had a lower cost base and could always beat them on price, even on stock and range, but they couldn’t match the experience of visiting the biggest toyshop in the world, right in the middle of London and all the fun that went with that.

Again this is something that we seem only slowly to be coming to terms with in telecoms: that price doesn’t keep customers loyal – there’s always someone cheaper, and over time the price differentials get smaller and smaller. Nor does technology and products – any new product is quickly matched by rivals, particularly in these digital times, and rarely justifies switching.

What really differentiates a telco – or any other company – is the customer experience. This is slower and harder to develop, for sure, but is also much harder to imitate, which in the long term makes it a much more effective way of generating customer loyalty and spend.

The telco’s interactions with its customers, at critical points in the customer lifecycle, are likely to be much more influential on their loyalty and their inclination to spend than a discount of a few percentage points. As a customer, how I feel about my telco is more likely to be influenced by how fast and how accurately my new handset or DSL line was delivered, whether it worked first time, how quickly customer service responded to my query, whether they knew what products I had and how I used them, whether they offered me an upgrade to a new handset without me having to ask… by any one of dozens of possible interactions where the telco has a chance to impress – or disappoint me.

So what did I take away from listening to these pieces?

Telecommunications is an increasingly open and competitive business – telcos compete not just with other telcos but with many other providers of apps, content and services. Utility-oriented business models and supporting systems won’t cut it any more.

New business models are needed if telcos are to be competitive in this new world, but maybe there’s less to fear than the industry sometimes seems to think, as whatever issues we’re struggling with, other sectors have often been there already and have found ways to be highly successful. In processes and systems there’s a lot we can learn, and maybe copy, from the wider economy.

Posted: September 3rd, 2010 | Author: OSS Team | Filed under: Around the World | Tags: bill shock, DNA, LTE, policy management | Comments Off on Around the World

Light Reading…

Telecom Market Spotlight: Asia

From a point about midway in 2010, Light Reading’s Market Spotlight looks both backwards and forwards at the Asia region. It updates the third-quarter estimates for the 2009 figures used in the previous Telecom Market Spotlight: Asia with now historic figures for 2009, and it includes estimates / forecasts for 2010. Focusing on the Asian market, the report touches on the following topics:

It contains a lot of interesting information and compelling statistics about the region. What is particularly fascinating to us is the special focus on ‘What happened to WiMax’. In Asia, there has been a trend among operators shifting from WiMax and moving towards a LTE environment. Light Reading surveyed the scene a couple of years ago, and it seemed that WiMax was the sure leader, but not so much anymore. The result is partly due to the much wider deployment of established 3G technologies (particularly HSPA and now the enhanced HSPA+) and the resulting smartphone boom, and partly of the rapid acceptance of 4G LTE mobile as the preferred evolution to next-generation technology by most of the mobile industry. Another problem for WiMax the report references is that WiMax operators are increasingly open to switching to LTE when doing so is necessary and economical—check out LTE Watch: Yota Drops WiMax for LTE.

Connected Planet…

Q&A: Verizon On Why QoS and Policy Matter

BSS/OSS reporter, Susana Schwartz recently caught up with Naseem Khan, principal member of technical staff at Verizon Labs, to get his company’s take on policy management. Given the conversation, it seems that quality of service (QoS) is top priority for Verizon, as they believe it will give them the competitive edge in the industry. Khan states that QoS will be a key differentiator in the industry and if there can be standardization of policy management around QoS, [Verizon] thinks it will help with managing multiple services and applications on the network — IPTV, data and voice — not to mention all the different access technologies. When asked about hindrances he sees ahead, he believes that time to market could be expedited if vendor platforms interwork through common standards—standardization is just the first phase, and then implementation by vendors is next. Recognizing this, Comptel designed a portfolio of OSS solutions—Comptel Dynamic OSS—to help CSPs realize their growth ambitions, and achieve their service creation and delivery objectives.

Policy management certainly seems to be on the minds of North American operators, as Susana spoke on this topic earlier with Farooq Bari, lead member of AT&T’s technical staff.

TM Forum Online Community…

CSP Gives Itself ‘Bill Shock’

A TM Forum online community member shares that Australian CSP, Telstra, incurred as much as AU $90 million in bad debts in its past financial year, caused largely by customers that disputed and didn’t pay expensive bills. Telstra’s chief financial officer, John Stanhope describes the situation as “…a customer might be described a plan, but when they get their first bill it’s hard to understand or doesn’t match the plan they thought they were going to get as described by someone at the front of house. Then a dispute occurs with the bill”. Apart of Telstra’s ‘simplification strategy’ is to make sure that customers understand the plan they have and how it will look on their bill. Wouldn’t a simpler plan involve a customer defining its usage limits? For example, take Finnish CSP DNA Ltd—it deployed Comptel Roaming Cost Control, which allows subscribers to monitor their balances in real time, and notify them of any necessary actions, such as a notification or suspension of the services when a specified cut-off limit is reached—avoid any unnecessary ‘bill shock’.

Posted: September 1st, 2010 | Author: Bob Machin | Filed under: Telecom Trends | Tags: customer experience, policy control, QoE, QoS | 1 Comment »

At Comptel we spend a lot of time talking about the ‘new business models’ that telcos are adopting to face a new generation of communications, and how these are likely to affect their OSS and BSS. But listening to the UK business news this morning made me wonder how many of our challenges are actually new, or unique to the telecoms industry.

This two part series will look at some surprising similarities between the business challenges under discussion and some key issues of the day in telecoms.

The first piece concerned Tune hotels, a chain that offers ‘5* hotels at 1* prices’. Tune has just brought its proposition to London. It consists of a basic room with a shower for a low, low price – averaging around £40 to £50 for a double room. Though you’ll pay more at weekends and other busy times, these prices are pretty good for London, where a single room in a 3* hotel would typically set you back over £100.

The rooms look clean and decent, but for your money, that’s pretty much all you get – a room. Anything extra is, well, extra – and not just breakfast. You want aircon? There’s a charge. TV or WiFi? Ditto. Towels? Toileteries? They don’t come for free either.

So it’s the budget airline model. You can keep it cheap if you’re determined and self-sufficient, but most people won’t and will rack up the bill with those many extras.

Listening to this, I couldn’t help thinking about the very similar issues we face in telecoms – in particular, how to attract and retain the customer in a competitive market, while at the same time turning a profit on our costly investments.

This seemed like a great example of a service that did all that. Customers can genuinely personalise and tailor it to their own needs and preferences, so they feel like they’re getting a good deal, a good service and that they’re in charge of their spending. Most importantly, it allows Tune to offer a great headline price while still turning a profit and to fully exploit the resources at their disposal. So how do they work this magic?

Their business model requires a flexible tariff, with many individually priced components and rates that can be easily changed, in response to shifts in the market. It requires a customisable offering – so that they can easily add or change the items available to the customer. It needs to let the customer self-configure their service and see it fulfilled on demand with minimal human intervention (got to keep those costs down!). It needs to support payment in advance and in real time – and immediate charging for those extras that suddenly seem important when you’re in the room.

As with budget airlines, it also needs to recognise and balance demand for, and availability of, resources – or ‘rooms’ as they call them in the hotel business – and control and exploit those two forces, with charging that maximises return in peak times and occupancy in off-peak times – or what we in telecoms like to call Policy Control.

So Tune seem to be well down the road towards effective control and charging which can balance the often competing forces of supply and demand, availability and price, in a way which attracts customers and turns a tidy profit. Are the legacy chains of established, incumbent hotels looking over their shoulders at Tune? You can bet they are…

In the next post I’ll look at the other item that was covered in that bulletin – what Buzz Lightyear has to tell us about how you hang on to customers and business in recessionary times… Stay tuned.

{kind=link}