Here’s an existential question: if you don’t think or talk about the Internet of Things (IoT), do you even exist?

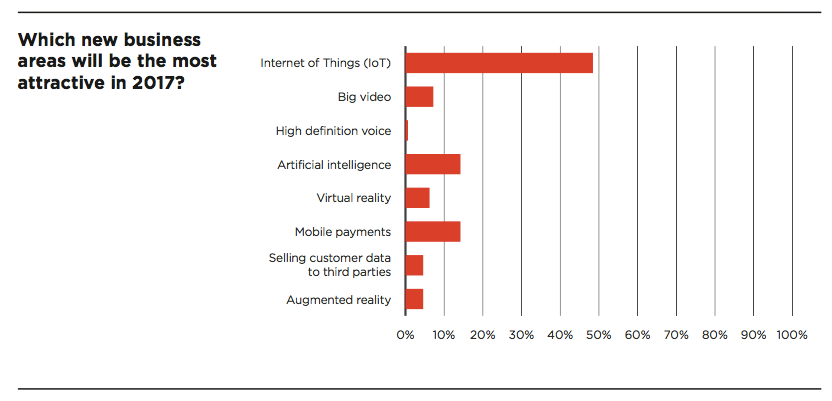

With the increasing number of IoT use cases on display at telco events, that could soon be the reality. It’s no surprise to hear that, according to the findings from the Mobile World Live Annual Industry Survey, IoT is the most attractive new business area for businesses in 2017. IoT, together with 5G, NFV/SDN, artificial intelligence, analytics, and automation, was among the most frequently discussed, debated and showcased topics at this year’s Mobile World Congress.

Discussions at MWC17 focused not on IoT theory, but rather the practical development of IoT applications and solutions, along with tangible real-life use cases. IoT solutions are expected to make life easier, healthier and smarter, and help to conserve the scarcest resource in an individual’s life: time. The solutions keep cities cleaner, safer and more secure. Tens of billions of sensors and connected devices will allow the digital economy to impact every aspect of our lives and improve the quality of life.

A number of these use cases were on showcase at MWC17, ranging from health services to IoT-enabled camera drones, location services to smart lighting, fitness to augmented reality/virtual reality (AR/VR), smart factories to connected dogs, and autonomous cars to self-service retail stores, to mention a few. Never before MWC had exhibited so much IoT, with leading Tier-1 operators demoing a range of practical solutions including a theft prevention solution for cars, mopeds and bikes, smart rubbish collection, livestock tracking, remote city lighting control, and remote health monitoring.

The conversation also revolved around the IoT network, including looks at LoRa, Sigfox, NB-IoT, LTE-M and 5G. 5G was heavily discussed throughout MWC17, in particularly in relation to certain IoT use cases like driverless cars, robo-taxis and remote surgical operations that mandate ultra-low ’millisecond’ latency, vast amounts of data, and frictionless, stable and high bandwidth data speeds. For example, Renault-Nissan has set a goal to roll out 10 car models with autonomous driver functionality by 2020. At the same time, LoRa Alliances and Sigfox are both rapidly expanding globally: LoRa, with its 400+ strong member alliance, has 34 publicly announced operators and Sigfox is already available in over 30 countries.

Discussions around advanced sensor technology noted the remarkable size and duration of the batteries that power these devices. IoT-enabled sensors are extremely small, but their batteries can last for up to 10 years, enabling the long-term monitoring of movement, location, temperature, skin moisture, activity, blood pressure, heart beat and many more factors. We also learned about a new material called Graphene – invented in 2004 and later the subject of a Nobel prize in physics – that enables the development of entirely new active sensors that could even be installed inside the human body.

Far away are times when MWC was just a showcase for telecom technology. Other industries presence has become a norm, the IoT is enabling the creation of intelligent and connected systems that will mean the entry of more new players, startups and industries at MWC. Car manufacturers, financial service providers, media companies, medical companies, smart city operators, transportation companies, retailers, industrial companies, agricultural entities and many more are involved or starting to get involved as they try to get their hands on with the latest transformative IoT solution.

At the same time, operators certainly need to talking to those businesses to seek new avenues of revenue growth. By enabling digital services for IoT, telcos can dramatically expand their number of potential customers enjoying digital services. In time, operators will see, meet and cooperate with many more of these use-case driven players in events like MWC.

By Niilo Fredriksen, Executive Vice President, Intelligent Data

A word of caution for all mobile operators: there’s a 50/50 chance your customers feel like you don’t actually care about them.

That’s what Comptel found when we commissioned a survey of 2,000 mobile data users in the US and the UK. Our new research report, The Power of Personal, reports that 52 percent of mobile customers feel like they are treated as just another nameless subscriber by their providers.

Obviously, that’s a problem that could lead to churn. Customers that feel valued are three times more likely to stay loyal to their provider, according to our research. Those that don’t feel valued leave, and 59 percent of respondents said they were not fully satisfied with their providers.

So how do you make sure your customers are happy, loyal advocates for your business? Personalisation offers a solution, and the survey found that it’s what mobile customers want from their providers.

In total, 55 percent of respondents said they would be open to receiving more proactive, personalised messages and services from their providers. But, only 13 percent has ever received this type of message.

Respondents said they were favourable to receiving all sorts of different messages, including:

An alert when they’ve reached their data cap

A notification when they’re about to trigger data roaming charges

A message when they’re using more data than usual

But it’s not just about warnings and alerts. According to our research, customers are also open to personalised messages about service offers, whether it’s a discounted data plan, sponsored data plan or a completely tailored plan that fits their exact needs based on service consumption. The key word, though, is personal. If you send customers an offer that doesn’t seem relevant to them, you’re not going to achieve anything but annoying them.

Service providers know a lot about their customers. It’s high time they started to use that data more intelligently to provide better more individualised services and to use that information to save customers money and build much longer lasting loyalty than is the current model. Our report gives you the guidance you need to do that.

Comptel Offer Example Templates to the Open Marketplace

State-of-Play

There remains no doubt that virtualization is shaking the foundations of the telecommunications industry and is here to stay. As the technology continues to mature and evolve, use cases become more realistic and so do the requirements to represent the service specifications that allow their programmatic utilization and consumption.

Several standards organizations have laid proposals to this purpose and there appears to be consensus that, in the Network Functions Virtualisation (NFV) case at least, TOSCA NFV appears to be positioning itself as the preferred option for operators and vendors alike.

The Topology and Orchestration Specification for Cloud Applications (TOSCA) is a data model standard managed by industry group OASIS that can be used to orchestrate Network Functions Virtualization (NFV) services and applications. TOSCA does this through a collection of information models and templates to orchestrate applications seamlessly across multiple cloud domains which is ideal for network functions that are virtualized and deployed in datacentres.

[Comptel] has taken the information that’s publicly available and created some examples that we would like to share with the broader community.

Use Case: vEPC Core Network CSAR

A basic representation of the Evolved Packet Core (EPC) Network Service Descriptor (NSD) composed of four Virtual Network Functions (VNFs) as shown in Figure 1 below. In addition, every node has a connection to a common management network.

Figure 1: vEPC Architecture & Interfaces

The CSAR file contains metadata, the service templates or specifications, images and the corresponding scripts for the VNFs themselves. Figure 2 shows the structure of the file.

Figure 2: CSAR file structure

As displayed in Figure 3, the metadata file contains in line 4, a pointer to the main driving template, in this case the overall vEPC NSD which will link to the individual nodes (e.g. VNFs) and their relationship and corresponding connectivity.

Figure 3: Contents of metadata file (TOSCA.meta)

The Network Service Design

The NSD provides the global overview (refer to snapshot below) on how the different components (e.g. VNFs, VLs, FGs, etc.) come together. Lines 9 thru 13 point to the VNF templates, in this case for every VNF.

The individual VNFs are described in lines 26, 37, 49 and 58 respectively. They contain a reference to the type, the list of (virtual) networks they are connected to and in those cases where applicable, a declaration of the forwarding graph capabilities (e.g. lines 45, 46 and 47). Additional details on the VNF themselves are contained on their own descriptors (VNFDs) which are shown later.

Next are the details of the external connection points (CPs). These are demarcation points for the NSD as depicted in Figure 4 and they are described in lines 65, 73, 81 and 89.

Figure 4: External Connection Points

Finally, the networks interconnecting the VNFs themselves. In this case, all networks are point-to-point connections (e.g. ELINE) except for the management one, which is shared across all VNFs (ELAN). Every declaration, as seen in lines 97, 108, 113, 119, 125, 131 and 137 indicates the number of network entities attached to them.

The Virtualised Network Function Descriptor

The VNFDs provide details on the specifications of the individual nodes. The vPDN GW descriptor is shown below as a reference. Starting on line 42 the connectivity is described. This VNF requires two computational resources as expressed on line 48 (VDU1 & VDU2). Two of its interfaces (CP21 & CP22) are enabled to support Forwarding Graphs (line 51). In this specific case, four standard transactions types are supported through self-contained scripts: create, configure, stop and delete (line 54). The interfaces and their respective networks can be appreciated in general the topology depicted in Figure 5.

Figure 5: PDNGW_VNF Topology

At the end of the VNFD template are two Forwarding Paths (Line 144 and 151). They represent the incoming and outgoing traffic for the PDN gateway. Figure 6 and Figure 7 provide a visual perspective of the traffic flows they control.

Figure 6: Forwarding Path1 on VNFD

Figure 7: Forwarding Path2 on VNFD

NSD_vEPC.yaml – File contents:

vPDNGW_VNF.yaml – File contents:

Comments

The standards provide enough tools to cover the most general of use cases, but we expect to see future updates that can target elements of the service description that represent more complex and realistic scenarios, for instance:

Quality of Experience (QoE) or in general Quality of Service (QoS) features. There are some brief references in the existing standards but this area requires further development.

The transactions/interfaces need to support more complex features that can allow them to be referenced and consumed more easily by higher order service orchestration processes.

Forwarding Graphs should include indications of the traffic types.

Although Comptel has worked out these areas for its own products and specifications, the real value materialises when these specifications become open and seamlessly interchangeable by the different components in the architecture.

Every great journey has a destination. In a business journey, your ultimate goal should be to find new strategies, ideas and approaches that benefit for your customers. The cloud might be the biggest such destination for many businesses in the telco industry today, and at Comptel, our cloud journey is about embracing the emerging platforms and solutions that will make life easier and better for our customers.

Comptel’s cloud journey took another big step forward at this year’s Nexterday North, where we announced the addition of another cloud solution, Fastermind. Everything about Fastermind is influenced by or tailored for Generation Cloud, the savvy digital natives whose buying and engagement preferences are changing the ways telcos have to service their customers.

Generation Cloud wants services on their terms, at their speed and personalized to their specific wants and needs. The cloud is the only way to deliver the dynamic, personalized services these customers crave.

As an industry, the benefits that we have realized by cloud adoption is unquestionable. We are on a journey powered by the cloud for our infrastructure, engagement and business models. Therefore, a well-balanced cloud strategy that drives focus back to business top-line and in parallel drives up the cloud maturity is needed.

The cloud has opened new business models that weren’t feasible in the past. It accelerates partnering, experimentation and building of ecosystems. But, it also creates complexity and dilemma with all the options that are achievable – stretching from NFV/SDN to private cloud to public cloud applications and hybrid environment, from do it yourself options to SaaS options.

Service providers are on a road to cloud. Many service providers have matured their cloud infrastructure strategy and have collaborated with their vendor partners to deploy solutions in the cloud and have demonstrated clear efficiency gains.

So, what’s your cloud journey look like? Are you running at the speed of business? Are unlocking new revenue streams? Is stakeholder engagement better than before? Do you have free hands to experiment new propositions? Even a small tweak to a service has a significant positive impact to the top line and experience.

Future success relies on being proactive and open to engaging as a part of a broader ecosystem. Cloud as an engagement model is bringing businesses closer so they can collaborate and win together. Cloud native strategy will bring the needed maturity. Cloud directions taken today with the focus on future proactive needs is a road to cloud!

At Comptel, we love the cloud. It brings us closer to our customers than ever before. We have been on a cloud journey for a long time already, as our operator customers serve more than 300 million end-customers in the private cloud environment. To date, our cloud solutions have provided our customers with important improvements in efficiency, but our upcoming product roadmap includes several important steps that will help us draw even more value out of the cloud. Stay tuned for more, and share your cloud journey!

Consumers want faster internet. Operators want to offer it. And now, regulators in the United States say they want to give telcos the tools to deliver it.

This month, the Federal Communications Commission (FCC) announced it would open up a range of spectrum – 28 Gigahertz, 37 GHz and 39 GHz – for the creation of the next generation of wireless services. 5G connectivity will represent a “quantum leap” in wireless capabilities, said FCC Chairman Tom Wheeler, because it promises to deliver speeds at least 10 times and possibly 100 times faster than 4G LTE.

The U.S. will be the first country in the world to open up spectrum for 5G, and there are many positive takeaways from the FCC’s announcement. First off, releasing radio spectrum is an obvious and important first step toward innovation. It creates a great opportunity for first-movers to start testing and developing new wireless technologies.

Wheeler also points out that the high-frequency bands now available to telcos support much higher traffic throughput compared to existing licensed spectrum, which will give “fibre-like” traffic capacity to wireless users. That will allow operators to dream up intriguing new services and applications.

There’s a lot to like from the FCC announcement, but of course it’s just the first step in the ongoing development of 5G. There’s a lot of work left to do to make 5G a feasible and profitable option for operators.

A Complex Regulatory Environment

Communication services providers (CSP) and network equipment providers (NEP) will need to make substantial investments to roll out 5G across the world, and they’ll need to do it fast to meet consumer demand. How will they recoup the costs of their investments?

One strategy might be to sell premium 5G-enabled services at a premium cost, but of course, those operators would need to be careful not to defy net neutrality regulations and expectations. There’s friction between regulations and operators on this issue. While FCC has ruled in favour of net neutrality, major U.S. telcos have argued that an inability to create priority services limits the funds they’d use to invest in infrastructure.

This issue should only become more pronounced with 5G. How can regulators and operators meet in the middle? There are a number examples of differentiated service models that balance private and public interests while working in parallel, such as public libraries and private booksellers, or VIP services in the hospitality industry. Regulators and operators must create an environment that encourages equal access but also offers unique opportunities for differentiated service models.

A New Infrastructure for Better Latency, Connectivity

5G connectivity is supposed to offer the network speed needed to power next-generation applications, the types that can’t afford lags or gaps in connection. A connected car, for example, needs fast internet access all of the time, whether you’re driving in a crowded urban environment or a sleepy rural community.

But solving for network speed is ultimately more of an infrastructure problem more than it is about adding spectrum. User devices will need to be moved closer to the edge of the network, which means a massive deployment of unobstructed antennas – that’s where the biggest costs related 5G deployment will be found.

How will that impact the future development of cloud infrastructure? Will it push us even faster toward global urbanization, with fewer people living in rural communities? How will investment in 5G be balanced against investments in faster fixed connections, like fibre?

Interestingly, many of the most popular use cases for 5G seem to suggest that, in the future, we’ll mostly access the internet via mobile networks. But of course, that’s not nearly the case across the world. In the United States, only 20 percent of households access the internet exclusively through mobile networks – 75 percent get it from fixed connections, according to the NTIA.

Now, the numbers are in fact slightly trending toward more mobile-only connections and fewer fixed connections in the US market. Globally, mobile broadband connections are, on average, 1.7 times cheaper than fixed-broadband, according to the International Telecommunications Union. But will operators choose to invest in both areas evenly, or favour one connection over the other? The most realistic vision for 5G connectivity might be in heterogeneous networks, a combination of wireline and wireless, where operators will be able to exercise a variety of connectivity technologies, including 5G, to deliver maximum service and experiences to customers.

Spectrum is one important piece of the puzzle that is 5G, but it’s still early days. The telco industry needs to work with regulators to solve issues around differentiated service offerings, and operators need to determine how best to change network infrastructure to support futuristic bandwidth-hungry service and applications.

Most software is built in layers. At the bottom sits the technical foundation, while at the very top there’s a user interface that connects man with machine. Most software users never actually deal with the technical layer – they’re happy as long as the software’s foundation works efficiently and as it should.

Instead, most user interactions occur on the surface layer, but that’s not always where developers and businesses focus their attention. A lot of development time is spent shoring up a product’s technical foundation, and while it’s very important to create a functional product that’s built on strong footing, a subpar user interface is not enough. Users need more than that. And a major challenge is that a product’s usability is invisible by nature and usually only gains attention when something is missing.

The User is Number One

What is usability in a nutshell?

The essence of it is to think about the usage of a product or service from the user’s point of view and consider the optimal way of interacting with the product to achieve maximum end-user benefits. It’s about enabling the use of a product or service to be as easy, as pleasant and as efficient as possible. It’s about simplifying complex things.

Users need products that are easy to learn and to use, that eliminate error-prone conditions, that create meaningful experiences, and, not to forget, that are pleasant to look at. Products need to make sense and answer the needs of users.

Users want products to be as fluent as possible, saving their time and, in the corporate world, saving their money. This need is universal no matter the software’s target group or ideal customer, whether it’s a private individual or a big global telco company.

So, how do software developers get to the point where their product’s users enjoy both maximum technical performance as well as great product usability?

One has to bear in mind that great product usability, as abstract as it sounds, is not a complementary asset – it’s an integral must-have quality for any service or software. The process of ensuring a service or software has the best possible usability goes alongside the whole development process, from requirements gathering all the way to delivery and beyond.

A Focus on Usability Saves Money

It’s not only end-users that benefit from an integrated approach to addressing software usability. Developers and businesses stand to benefit, too.

By utilizing user-centric design methods from the beginning, it’s easier for developers to track what customers want and compile a comprehensive list of product requirements. In fact, it would be beneficial for all parties, if possible, to have continuous communication between customers and the user experience design team to track satisfaction with a product’s usability and features.

After feedback is received and new product requirements determined, continuous end-user feedback and validation during the design and development stages will ensure faster progress and earlier resolution of design flaws or feature missteps. Failing fast saves development time and money.

How Comptel Addresses Product Usability

The Comptel user experience design team utilizes user-centric design methods that aim at taking the end-user into account from the very beginning of the design process. The range of different methods is vast, varying from user interviews to focus groups, workshops and co-creation. End-users and experts are an integral part of the design process and their knowledge is being utilized at all phases. We aim to achieve continuous dialog with our end-users.

Usability Can Also Be a Competitive Asset

Let’s not forget that Comptel is not the only business operating in the area of telco software development. We always ask ourselves: How can we differentiate from the other providers in this highly competitive environment? What makes us better?

When a software’s technical performance, feature list and price are approximately on the same level, it’s the surface-level usability that makes the difference to customers. So we work to deliver a superior user experience that customers know is quintessentially Comptel.

You can’t create a world-leading software product without offering both great technical performance and a great user experience. And you can’t deliver a great user experience without supreme product usability. These factors combined equal quality. And quality is our key driver.

The story on convergent charging has been a simple one: operators are adding more subscribers and a wider range of dynamic digital services, and thus need to transform their networks to support that. Billing and charging are important components to the infrastructure, and convergent charging is a way to achieve simplicity and flexibility through consolidated payment.

When you can create a single bill or account for all your disparate services, including fixed telephony, prepaid and postpaid mobile, SMS, data services and more, you create a better, more efficient experience for you and your customer.

Again, it’s a simple story, which is a big reason why the most recent numbers from Infonetics Research reported that convergent charging is a $3.1 billion global market. However, given how quickly the telco market changes, it’s worth stepping back to evaluate how the evolution of consumer demand has impacted the supposed emergence of convergent charging.

One important factor is the increasing business irrelevance of the traditional communication services, voice and SMS. Voice, we know, is a rapidly declining business, experiencing reduced customer usage and reduced revenue as a result. SMS, similarly, is being offered as part of unlimited bundles with voice.

And we all know what’s happening with data – it’s exploding. All the innovation around revenue generation and service creation is happening in the world of data. We’re observing entirely new data-driven service models that put access to digital content, like over-the-top (OTT) services, at the centre of customer packages. Voice is even being gobbled up by data – just look at the emergence of VoLTE, which has been launched in 55 live deployments in 34 countries, according to the latest figures from the Global Mobile Suppliers Association (GSA).

At the same time, we often hear all about the disruptive BSS transformation needed to provide a more flexible and convenient customer service experience. So, with data the clear-cut leading horse for revenue generation and service innovation, and radical BSS transformation changing customer service expectations, what does that mean for convergent charging? In fact, is there even any point in trying to converge these services into one system, when two of the three won’t provide much in the way of revenue at all in the near future?

Convergent charging was all about merging payment methods and services to benefit the end user. A user could choose to pre-pay, post-pay or mix payment methods, and a single system would be able to manage it all, instead of the two or more systems operators previously relied on. The question is, have consumers adopted hybrid payments – the key reason for payment convergence at-large – or are we naturally using the payment method of choice irrespective of the services we consume?

Has convergent charging, as we know it today, become an obsolete concept? Are current convergent charging platforms built to serve a stale and irrelevant market view?

The telco industry is experiencing a massive BSS transformation, and convergent charging is an important part of it. Modern convergent charging platforms will need to enable innovation in multitudes of services, but in three or four critical domains: shared/single quota management, sponsorships/third-party pays, data consumption and the transition of voice to data (VoLTE).

Shared/Single Quota Management

The average digital consumer owns 3.64 connected devices, according to GlobalWebIndex. That number should only continue to grow, as consumers want to stay plugged in to their favourite apps and digital services around the clock. Operators, then, should want to converge payments for all the services on these devices into one central bill or account.

A single multi-service account, in which a customer has one common account for multiple services, is a clear use case for billing convergence. In this scenario, an operator would offer master account handling with convergent quotas and quality of service management (QoS) across multiple channels, including mobile, Wi-Fi internet, cable TV and across a growing number of devices.

The problem is that initially planned convergent charging platforms require an expensive architecture that is not designed for the dynamic and agile associations of devices to accounts over complex fixed and mobile networks. As a result, these systems cannot find a simple way to enable concepts like family payment plans or the single management of streaming content, like Netflix, on a tablet device that can dynamically switch between cable-provided Wi-Fi and cellular-provided internet access.

Third-Party Pays

Another clear opportunity for next-generation convergent charging is in solving some of the asymmetry around third-party pay concepts, and offering two-sided B2B2C business models.

At TM Forum Live! 2016, Comptel was part of an award-winning Catalyst presentation sponsored by Orange. The Catalyst offered a view of sponsored data payment models, in which a corporate sponsor of some kind could build sponsored data packages for an operator. The result would be that customers receive free data access, the sponsor receives an opportunity to market to the customer, and the operator receives a fresh new wholesale revenue opportunity, increased data consumption and improved customer loyalty.

This model could introduce a complex payment structure – rather than being paid directly by the customer, an operator could technically be paid by multiple parties. Traditional convergent charging platforms don’t have the flexibility to support this modern payment approach, and cannot offer the valuable personalised customer engagement and marketing capabilities needed to make this model successful. The sponsor would expect lead generation capabilities, and the operator would need to create a real-time, zero-touch, closed-loop consumption model that includes marketing, sales and service delivery.

That’s what you get from new BSS, convergent charging platforms and innovative solution – the ability for the sponsor to define the sponsorship packages and the system providing them, the ability to find and qualify the ideal customer for a sponsored data package, and then deliver that package to the customer automatically, without operator-induced friction.

Data Consumption

All signs point to user data consumption shifting. The 2016 Internet Trends report from KPCB underscores the acceleration of streaming video. While just three years ago, semi-live content, such as Snapchat stories, were the new frontier in mobile content, today’s big platform is real-live content. Consumers love mass audience experiences like Facebook Live or Periscope video, which allows any consumer to stream live-video to the network and for audiences to watch real-time video in the moment.

This is only the start. At Mobile World Congress 2016, Facebook’s Mark Zuckerberg said the future belongs to video, in particularly to users the streaming 360° video that underpins virtual reality experiences to the network. This behaviour is a major shift – users have gone from downloading video to uploading real-live video.

Transition of Voice to Data (VoLTE)

Although VoLTE will not be a silver bullet solution to voice revenue, it can be a step toward real-time communication on the Web (WebRTC). The upshot is, operators are moving toward a future where all of their services are delivered over data. After a period of time in which consumer devices migrate to VoLTE, this will enable operators to minimise the circuit-switched infrastructure and potentially even shut it down someday.

Convergent charging, then, will really be all about converging payments from different sources – not just the actual mobile customer. Instead, operators will need to converge payments from the different data-driven services and systems that underpin consumer services of the future. This requires fresh thinking to transform BSS to correspond these new requirements.

Converging Toward Living Data-Driven Services

Transitioning to convergent charging, to date, has meant expensive and complicated BSS and architecture transformations. However, market forces are making the traditional motivating factors behind that kind of convergent charging obsolete. Instead of thinking of ways to combine voice, SMS and data and to enable hybrid payments, operators must move past traditional communications services. They should embrace a future built on data and BSS transformation, along with the flexibility to create dynamic business models and living services that are offered to customers at the perfect time.

By Stephen Lacey, Principal NFV Architect, CTO Office & Guest Author

Comptel was in attendance for the second annual NFV World Congress, held last month in Silicon Valley. Whereas the discussions at last year’s inaugural event were more academic in nature, this year’s conference showcased a number of compelling cases that demonstrate how network functions virtualisation (NFV) is taking a step toward becoming reality.

The week kicked off with a series of tutorials from the Open Networking Foundation (ONF), the European Telecommunication Standard Institute’s (ETSI) Industry Specification Group (ISG) for NFV, and the Intel Network Builders (INB) – Comptel is a proud member of the latter two groups. Throughout the week, we also observed a number of presentations from operators driving home the reasons why they are exploring NFV implementations. Two reasons stood out:

The potential reductions in CAPEX/OPEX due to utilising ubiquitous general purpose hardware

The ability to achieve service flexibility and mix and match services.

NFV in Action

Japanese operator NTT offered a great example of the benefits of service flexibility. During a tsunami in 2014, the need for voice traffic capacity near the storm’s epicentre increased dramatically. There was plenty of capacity in the other parts of their network, so if NFV had been available at that time, NTT would have been able to offload data capacity to other parts of the network to increase voice capacity in areas that would have needed it most.

NTT was the only operator at NFV World Congress running two different virtualised evolved package core (vEPC) vendors on live deployments: NEC and Fujitsu.

AT&T, Verizon and the bulk of the operators speaking at the event said that virtual customer premises equipment (vCPE) for enterprise-based services is the most compelling of the NFV use cases for them. When pressed, AT&T described how their customers had surprised them in the way they utilise services.

By using the AT&T ECOMP platform and EVPN as the bridging mechanisms for Layer 2 and Layer 3 switching, plus allowing their customers to chain virtual network functions together, customers enjoyed time-of-day-based services variation. For example, during the workday all branch offices had equal bandwidth to access the main datacentres, whereas after business hours those bandwidth allocations were lowered and higher bandwidth was assigned for datacentres to sync together.

Other operators said they are entrenched in NFV trials, but didn’t offer any behind-the-scenes information as to how those programs are progressing.

The Emergence of Open Source

Another important theme was the increasing mainstream relevance of open source projects, which major network equipment providers (NEPs) and communication services providers (CSPs) are relying on to prevent vendor lock-in within the network.

It seems 2016 is the year of orchestration wars, with two different open source projects exploring this aspect of network management and organization (MANO): Open Source MANO (OSM) and OPEN-Orchestrator (OPEN-O). It’s difficult to directly compare the two initiatives, since OSM is based on available software, whereas OPEN-O is only in its foundational stages.

Nonetheless, it will be interesting to keep an eye on each initiative as they progress. Comptel recently participated in a partner showcase at TM Forum Live! alongside Telefonica, Indra and Etiya which proposed a hybrid network environment based on OSM.

NFV World Congress offered a compelling venue to explore how leading operators and vendors are actively experimenting with NFV implementation. As a few pioneering telcos embrace virtualisation within the network, these first forays will carve a clear path forward for the rest of the industry. Some will take the lead; others will simply follow.

By Simon Osborne, CTO Service Orchestration, Comptel

In the world of telco, emerging back office technologies – especially network functions virtualisation (NFV) – appeal to operators not just because of the promised evolution of infrastructure management, but also because of the potential difference these technologies can make to the bottom line.

It all starts and ends with digital services. We’re living in an app-driven world, where consumers build personalised ecosystems of apps and over-the-top (OTT) content. These customers are on the search for apps and services that solve specific problems or meet their unique needs, from personal health to entertainment and everything in between.

Businesses are the same way. Not only do companies want access to a wider range of digital capabilities – video and Web conferencing, cloud-based email and productivity software, connectivity and security services – but they also now expect a B2B buying experience comparable to the speed and personalisation they receive as B2C digital buyers.

How can operators deliver personalised, engaging service experiences to B2B and B2C customers? Through a conversational and automated service orchestration and fulfillment framework.

Comptel is partnering with IBM and Juniper Networks to develop just such an architecture. As a participant in IBM’s Cloud Based Networking (CBN) initiative, our aim is to leverage SDN and NFV technologies in the creation of an agile, self-service model for service configuration, validation and completion. We’ll share our new revision for OSS and dynamic digital service delivery with attendees and booth visitors at TM Forum Live! in Nice, France from 9-12 May.

Extending the Potential of NFV and SDN

Technologies in isolation don’t really change much about the state of play. The same is true for NFV. There’s nothing inherently disruptive about having a virtual version of a network function. Adding a “v” in front of OSS won’t mean you’ve revolutionised your business. It’s really about how you’ve applied that new technology to meet customer demands.

The real value of NFV is that gives operators the agility and flexibility to consider new ways to serve enterprise and individual customers. With a highly scalable, agile and flexible network, an operator can dream up and launch the innovative problem-solving services their customers want. In turn, the self-created apps and service ecosystem can drive new operator revenue streams.

The Model for Dynamic Self-Service Delivery

To bring this vision to reality, IBM is adopting Comptel’s Digital Service Lifecycle Management (DSLM) proposition. This NFV-driven model works across three layers: one for network orchestration, virtual function, IT and physical network management; a middle orchestration layer to manage end-to-end hybrid service orchestration and the digital service lifecycle; and a top layer for front-office customer engagement and business management.

Comptel’s FLOWONE V service orchestration solution will fulfil the central DSLM layer, while IBM and Juniper will provide the network domain and IT service orchestration, dynamic operations, customer engagement, DevOps and security applications and services. Through integration with a digital service catalogue, this three-tiered system is able to support fast and easy self-service product ordering and configuration at the customer level. The model accounts for automated validation to ensure service availability and feasibility, and includes intelligent resource management to ensure the system can scale for service demand.

In future blogs, we’ll dive into the market potential for this type of model and the technical aspects that make it possible. But for now, it’s clear to see the revenue possibilities for operators. With a smart, automated and self-service digital sales cycle, you empower customers to build their own personal ecosystem of digital services and apps. Agile NFV and SDN technologies let you deliver these capabilities at an attractive cost. Ultimately, this model presents an innovative way for operators to expand their service capabilities and unlock new revenue in the era of rising digital expectations.

Visit Comptel and IBM at TM Forum Live! to learn more about the IBM Cloud Based Networking initiative and our model for dynamic digital service delivery. Email [email protected] to schedule a meeting. You can also read more about digital service lifecycle management at Nexterday.org, our online magazine and reader community.

By Harry Järn, Head of New Business Ventures, Comptel NXT

Last week’s Nexterday North delivered big ideas from industry experts, business leaders and futurists who discussed the impact of digitalisation on our world. It also included one big surprise: the launch of Comptel’s FWD, a solution that we believe will revolutionise how operators serve customers in the next age of digital services.

What is FWD? It’s a full E2E, cloud-based, white-labelled, solution for operators.

The basic components of FWD, which includes SMPL, the native app, CTRL, the cloud-based controlling system and CNSL, the browser-based operator management tool, combine to create a complete solution for enabling and managing mobile data purchasing.

The native app radically simplifies how mobile customers purchase data. It puts customers in the driver’s seat by letting them set their own terms for buying data. It also puts operators in a better position to monetise mobile data at a time when customers desire more control of service terms and highly personalised, instantaneous service.

Our own mobile customer survey demonstrated why many subscribers are frustrated with the current state of mobile data purchasing. According to the report, 65 percent of consumers struggle to find a mobile data package that fully meets their needs, while 62 percent feel their mobile operator lacks a wide enough range of package options.

Part of that frustration can be tied to rigid mobile data packaging. Though they currently buy data by the gigabyte, customers aren’t sure just how much data they need. Is a 1GB package enough if you only plan to check emails and surf the Web? Is a 10GB plan economical for someone who watches streaming video on their smartphone?

FWD eliminates customer confusion by empowering mobile users to easily buy time-based data access. Here’s how it works: Let’s say a user wants to browse Facebook for just a few minutes. After he opens the Facebook app, he’ll be prompted with a few time-based data options, whether it’s one minute or one month of access. Once the data packet is purchased, the user is free to browse Facebook without limits, and he can easily extend his session if he needs more time.

That means no more bill shocks for surpassing their data overages. No more frustrating data throttling in the middle of a streaming television program or movie. No more complex, extended data service plans. It’s a simplified purchasing process that ties directly into customers’ desire for data control. Our survey found that 65 percent of mobile users want to set their own terms for buying digital content and services. FWD lets them do that.

The FWD management tool for operators opens up new possibilities to sell, target and market mobile data, as well as monitor your business performance in real time. You have full control over offer creation, which means you can experiment with new ways to entice your mobile customers. Embedded analytics will help you understand how your customers consume mobile data and allow you to react accordingly, which could mean dynamic pricing that helps you run a more efficient and profitable network. All of this analysis occurs instantly and in-the-moment, not after a month of data crunching.

We’re also excited about the possibilities FWD offers operators in tapping into a new market: the 2 billion individuals worldwide who have not yet been connected to the internet. With smartphone penetration expected to take off in emerging markets, the question of bringing all these new mobile users only will need to be answered. FWD provides a compelling solution because it’s easy to use, fosters customer engagement and loyalty, and encourages customers to spend more on mobile data.

Digitalisation is forcing many operators to re-think how they engage with and serve a new breed of mobile consumer. Comptel is excited to help operators innovate their service approach and drive toward a digital business revolution.