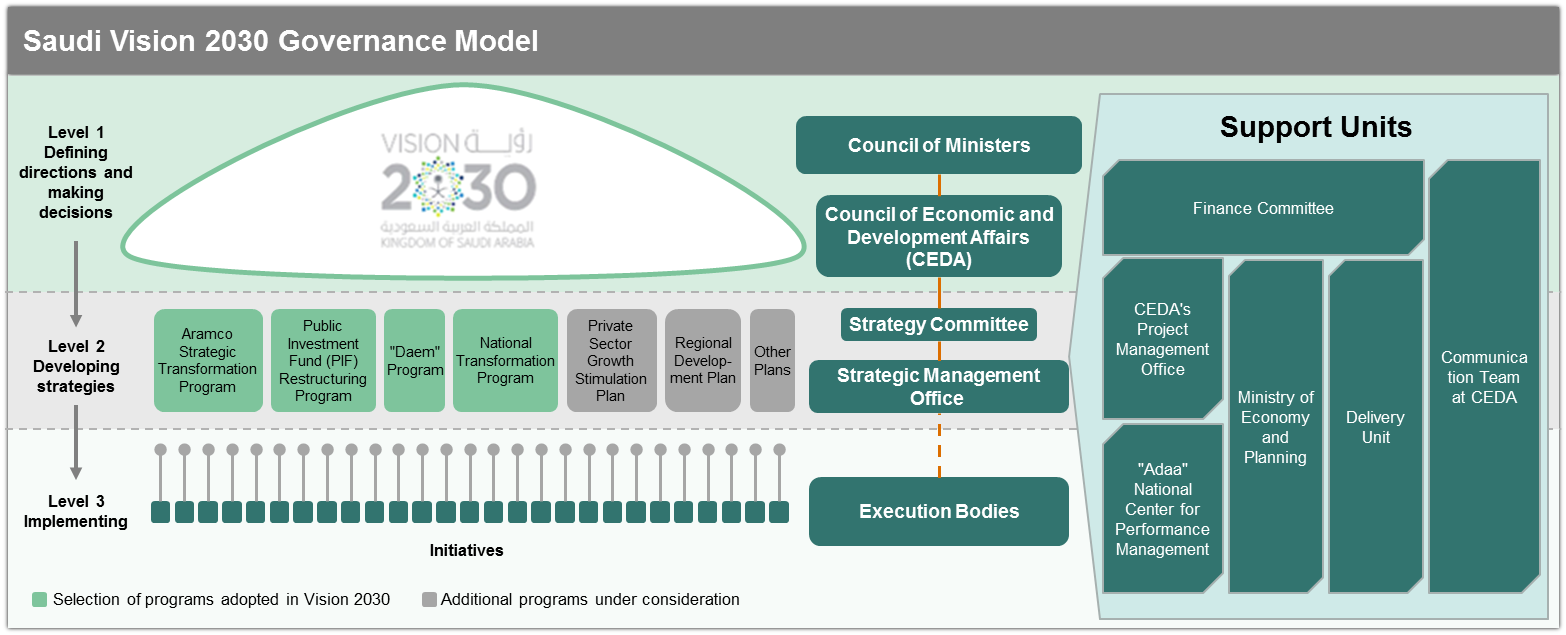

The Kingdom of Saudi Arabia has set itself on a future-looking transformational journey for its people, the country and the region. Aiming to leverage itself as an investment power, backed up by a healthy portfolio of rich natural resources, the Kingdom will be a driver to connect African, Asian and European trade.

To fulfil the vision, it will be focusing on three key themes – a vibrant society, a thriving economy and an ambitious nation. The importance of the vibrant society is supported by strong historic roots and national identity, a good standard of living, family life and a supportive social and healthcare system. With a thriving economy, the KSA aims to provide “opportunities for all by building an education system aligned with market needs and creating economic opportunities for the entrepreneur, the small enterprise as well as the large corporation.” But, it won’t happen without ambition, so the Kingdom will look at improving efficiency and responsibility at all levels – starting with “an effective, transparent, accountable, enabling and high-performing government.”

A number of programs monitored by strong governance have been designed to help KSA conquer their vision and more details can be found here: http://vision2030.gov.sa/en

STC Role in Vision 2030

In 2016, Dr. Tarig M Enaya, Senior Vice President of the STC Enterprise Business Unit, was interviewed by a leading Middle East technology reporter at ITP.net. In that discussion, Dr. Enaya explained the role that Saudi Telecom Co. will play in Vision 2030.

“Digitisation is at the core of Vision 2030, essentially meaning we have a key enabling role to play,” he said. “We own and operate the largest fixed and mobile networks in the Kingdom, meaning we can connect almost any populated location in the Kingdom. We have a 147,000km-long fibre optic network tying major cities together, interconnected with metro rings, and reaching smaller towns and villages. We patch cover some areas with microwave and other technologies. Our mobile network covers 96% of populated areas, with 85% of all populated areas having LTE 4G network coverage.

“More important for Vision 2030 is the integration between ICT services and how integrated services and solutions are delivered and supported,” he continued. “To accelerate the growth of any service, you need good business practices and flawless business automation, a variety of different systems from different government agencies need to be interconnected together, and most important systems have to have very strict SLAs and high up-times.

Dr Tarig M Enaya, Senior Vice President of the STC Enterprise Business Unit

“For us, Vision 2030 means we will continue to do what we have been doing since we merged the operations between our three business-to-business entities, the STC enterprise business unit, STC Solutions, and Bravo, but we will have to work harder and much faster.

Where things have dramatically changed over the past five years is how IT services are delivered, and the introduction of a cloud-based model and managed services methodology. When applied together to address customer needs and requirements, the two can create a very powerful mix. Virtualisation is the best way to manage IT hardware resource efficiency, but in its traditional sense, it means all the hardware is in one place, something that only the cloud can address.”

FUDEX 2017

The Future of Digital Technology Exhibition 2017 (FUDEX) was inaugurated by the Minister of Communications and Information Technology, Dr. Mohammed I. Al-Suwaiyel and organised by Saudi Telecom alongside major international companies in the ICT sector. The event (aligning itself to the KSA Vision 2030) took place 28th-29th March at the King Abdullah Petroleum Studies and Research Center (KAPSARC) in Riyadh. Its focus was to introduce the latest network/IT technology through an exhibition and workshops to the various departments of STC and the industry.

Exhibition

The exhibition was representative of today’s traditional telco thinking with a clear demarcation of network suppliers versus IT vendors. The network suppliers generally promoted around the key telco themes of 2016/17 – 5G, IoT and virtualisation, each being eager to promote their own proprietary solutions. The IT vendors focused specifically around application and data security, plus the enterprise deployment of IT applications in the cloud. The only obvious vendor-agnostic supplier of OSS/BSS offerings for telco services was Finnish independent software vendor Comptel.

The one observation that emerged from being part of and studying the expo was a distinct lack of network and IT convergence perspectives. The network vendors were discussing their own particular flavours of infrastructure cloud commoditisation, and the replication of traditional network features as virtual network functions (VNF). There was little attention paid by these suppliers to actual commercialisation of NFV services and the evolved processes needed. The IT vendors, on the other hand, demonstrated little to no appreciation that the CIO’s role is due a considerable responsibility upgrade as the network moves to a data centre model. No doubt this will be a focus for STC in the coming year and next year’s FUDEX will likely represent the convergence more strongly.

Ministerial VIP Visit

Along with a huge entourage, the exhibitors and attendees were treated to an Executive VIP visit from Minister of Communications and Information Technology Dr. Mohammed I. Al-Suwaiyel , STC Group CEO Dr. Khaled Hussain Biyari, and STC Technology & Operations SVP Nasser Sulaiman Al Nasser. The executives familiarised themselves with many of the exhibiting vendors being suitably impressed with the future technology and solutions being promoted to assist STC to address the challenges of the KSA Vision 2030.

Comptel at FUDEX

Since 2015, Comptel has been championing the vision of “Perfecting Digital Moments” alongside its thought-leading NEXTERDAY concept, which encourages the telecommunications industry to “Think Again, Think Ahead and Think Across” vertical industries. The concept aligned very well with the visionary objectives of KSA Vision 2030, especially around digital transformation and empowerment of its people through technology.

During the event, Comptel were promoting two Digital Journeys that telcos around the world are currently addressing. The “Digital Customer Journey” presents solutions to map out contextual engagement, service personalisation and customer experience to help the telco CMO transform and connect with valuable subscribers and consumers. The “Digital Service Journey” lays down a realistic approach to addressing the evolution of telco network services and IT/OSS. It considers the modernisation of telco operational processes and roles, the introduction of early-stage hybrid virtualisation technology, plus the move to full scale Digital Service Lifecycle Management™ for future-state NFV-enabled networks. This was the topic of the keynote workshop delivered by Comptel to an impressive audience from across STC attendees.

In addition, Comptel and STC announced a second initiative to nurture and develop young talent within Saudi Arabia. The first initiative in 2014 took a number of talented young STC IT professionals to various locations around the globe, educating them on the broader business and technology topics from the telecommunications industry. In 2017, STC and Comptel announced the “Hunt-a-Shark” initiative and signed a joint memorandum-of-understanding at FUDEX.

At the very heart of Vision 2030 lies innovation, youth enablement, cost optimisation and economic growth through new revenue sources. The “Hunt a Shark” contest is aiming to unlock these objectives by inviting university students from Riyadh to share their ideas about emerging digital platforms and artificial intelligence-driven economies. Finalists will compete to secure – or ‘hunt’ – seed funding, training and mentorship to support their ideas, based on business rationale, uniqueness, viability, relevancy and alignment of their idea with Vision 2030.

Summary

The Kingdom of Saudi Arabia are embarking on an exciting path with Vision 2030. They have the resources, the people and the ambition to get there and Saudi Telecom with its industry-leading partners will clearly play an important role to make the vision a reality.

Have the rules changed for Communications Service Providers to engage with their customers?

Digitalization has created a generation of empowered, engaged and demanding “Generation Cloud” consumers. These people want to be treated as individuals through using a service that meets their expectations and aligns to the way they live their lives. They don’t want to follow service providers’ rules but instead, define the digital market as they want to see it. Service providers have to identify product opportunities, then design and commercially publish new service offerings faster than ever. Only then will they be able to seize the increasing new opportunities for data, content, applications and service monetization. Effectively they have to monetize more in less time, whilst leveraging partner offerings for service enrichment.

How do service providers win the hearts and minds of customers with almost impossible expectations?

To meet the expectations of generation cloud consumers it’s no longer sufficient to have a static portfolio of products that a customer selects and uses unchanged for the lifetime of a contract. Lifestyles, demands and expectations create a digital opportunity for providers to continually engage with their customers with contextually relevant enrichments to a base package contract.

These enrichments or upsell opportunities can take the form of traditional data or messaging bundles, however they can now also encompass personalized add-ons such as streaming subscriptions or cloud-storage with a data allowance; time-based video streaming bundles and sponsored enterprise data packages. These modern-day enrichments have to be more understandable by the consumer, as lifestyle enhancements aligned to them.

Service providers have an opportunity to not only create these offerings but intelligently identify when to make a recommendation and with which product. They also have to simplify the engagement and buying process as closed-loop automation, allowing for consistent improvement, alignment and customer retention.

What would the perfect solution look like for CSPs to enable the personalised customer journey?

A comprehensive turnkey solution for the personalized journey will incorporate a number of steps that the customer service lifecycle will take. These steps consist of product creation based on identified market needs, campaign management and commercialization of those products, an ordering process and of course the delivery of a product in the first instance.

Once delivered it’s necessary to collect data and valuable information on the consumed service, which when analyzed provides insights to drive the intelligent recommendations required for next customer contact via a simple interaction or detailed marketing campaign.

Realizing that the recommended add-on is a perfect fit, the consumer then needs a seamless buying and delivery experience – leading to the creation of a revised automation-loop for continuous future engagement.

A Modern Day Customer Engagement Architecture

Leveraging a communications industry data integration framework, Salesforce, Apttus and Comptel are perfecting the personalized customer journey through a number of identifiable steps.

Designing – B2C or B2B service design based on technical network and service capabilities, with input from market research created by product management.

Commercializing – Publishing of the product as a commercial offering, allowing a customer to discover, select and customize to their needs.

Ordering – Submission of the selected and customized product as an order into the buying process. Incorporating CPQ processes (Configuration, Pricing and Quotation).

Delivering – Order processing and service activation plus an all-important notification to the subscriber for full customer engagement into the process.

Tracking – Continuous charging, metering and full reporting of service consumption by the subscriber, giving a 3600 perspective on contextual usage.

Analyzing – Contextual analysis on service usage trends of the subscriber leading to intelligent recommendation for product upsell and tailoring – customer alignment and engagement.

Growing – Perpetual engagement, offering continual recommendations to an individual and the option to buy. Perfecting the customer engagement process.

The Solution

The result is an eco-system primed solution for customer engagement and contextually-intelligent product recommendations, leading to automated customer lifecycle management. The solution is enabled by the Salesforce Communications Framework & Data Exchange, Salesforce Customer Success Platform, Apttus Quote-to-Cash solution and Comptel Intelligent Data Monetization & Customer Engagement Automation.

The tech leader rolled out the newest version of its smartphone last week, and by all accounts the latest iPhone’s features are mostly iterative than innovative. The most disruptive hardware change was also the one that frustrated consumers the most: the elimination of the 3.5 mm headphone jack, which requires iPhone users to use Apple’s proprietary headphones instead.

Similarly, the iPhone’s user interface seems to have plateaued. While the iPhone 7 will ship with a new operating system that includes a handful of new features, the look and feel of Apple’s UI is still virtually unchanged from where it was several generations ago. You can add some more pixels here and round off a few bevels there, but for the most part, iOS doesn’t offer much opportunity for further design innovation. Apple’s UI is what it is because that’s what its devout customers expect.

That’s not necessarily a knock against Apple’s UI. They’ve found an interface that suits its fanbase, and they’ve even inspired design innovation in other areas of software development. In fact, one software experience that’s long overdue for a fresh coat of paint and user-friendly functionality is OSS.

To date, we’ve seen OSS interfaces designed around the technology in the network: topologies, hardware representations and configurations that must be manually realigned based on user. However, the emerging app- and data-driven digital economy is putting increased pressure on operator networks to be agile, dynamic and automated. Meanwhile network function virtualisation (NFV) is changing the speed and nature of service orchestration by simplifying network processes and application deployment.

Doesn’t it make sense, then, that the OSS should be refreshed to enable an agile and more productive work experience for telco operations managers?

Telco is starved for a strong, functional and distinct OSS UI. The folks who support service orchestration vary in roles, responsibilities, skill levels and professional backgrounds. OSS UIs should be designed to correspond to that variety, so that each user is able to focus only on those operational elements that they are most equipped to manage. That increases efficiency and the speed at which digital services can be developed, verified, deployed and improved.

As a result, time-to-profit goes down, while customer satisfaction goes up.

That’s why the shift toward cloud-service operational management will bring an evolution to the OSS, in the form of tailored, intuitive user experiences and subsequently increased productivity. The new OSS will be open, capable of seamlessly interacting with both telco and IT apps and their corresponding management systems. As a result, telcos benefit from a higher order platform to specify, test, publish for consumption and deliver services across virtual, physical and IT domains.

An intuitive OSS UI also supports a seamless end-to-end service lifecycle, eliminating any gaps in the process by which network resources are discovered and services are designed and deployed.

Ultimately, the new OSS recognises that virtualisation is an opportunity for telco to reinvent itself. Operators can offer more than just a telecommunications platform – they have a chance to become part of a larger, distributed IT infrastructure that seamlessly provides services to end customers. Our existing OSS culture needs to evolve in order to recognise that this paradigm shift requires opening up the infrastructure to deliver services and resources in a more agile, open and systematic way.

Comptel will discuss the reinvention of the OSS user interface paradigm in The Hague for SDN & OpenFlow World Congress, 10-14 October 2016. Contact [email protected] to connect with our team or arrange a meeting at the event.

Posted: September 12th, 2016 | Author:Steve Hateley | Filed under:Industry Insights | Comments Off on Comptel and MEF: Shaping Service Orchestration for the Digital Economy

For the past 15 years, the MEF Forum has been focused on driving forward innovations in network performance to help operators deliver carrier-grade ethernet connectivity and more recently, what it calls “Third Network Services.” As one of 200 member organisations, Comptel is pleased to play an important role helping to shape MEF’s guidance around next-generation service orchestration with our Digital Service Lifecycle Management (DSLM) model.

Last month, Comptel took part in the primary annual meeting of the MEF member organisation in Boston, where we had a great opportunity to explore how our DSLM model for service orchestration complements MEF’s vision for NFV-driven service delivery and lifecycle management.

What are Third Network Services?

MEF describes Third Network Services as those that “combine the on-demand agility and ubiquity of the Internet with the performance and security assurances of Carrier Ethernet 2.0.” The organisation is essentially describing a variety of digital services that rely on optimised high-performance networks to meet the quality of service expectations of today’s digitally savvy Generation Cloud consumers.

Examples include performance-assured wired or wireless internet connectivity, which automatically optimises the performance of your network whether you’re working on a train, in your home or from a hotel room on a business trip. The Third Network also provides assured, dynamic network performance for businesses, enhancing the experience for each end user on each cloud application even if the company uses multiple internet providers across multiple offices.

The idea is to provide quality, assured service experiences that customers can control. MEF’s vision for Third Network Services closely aligns with Comptel’s own view of dynamic digital services, which is why we’re excited to bring our DSLM model to the table in conversations with MEF member organisations.

Developing LSO and DSLM

To enable these services, MEF has introduced a number of models and specifications that define how operators should evolve their networks and integrate emerging technologies, such as network functions virtualisation (NFV). Member organisations, like Comptel, take part in ongoing MEF initiatives and proofs of concept to engage with and develop these standards and models.

One such model is MEF’s Lifecycle Service Orchestration (LSO), which leans on NFV and software-defined networks (SDN) to streamline and automate “the service lifecycle in a sustainable fashion for coordinated management and control across all network domains responsible for delivering an end-to-end connectivity service,” according to MEF.

Comptel’s DLSM, which models dynamic service orchestration in an NFV-driven digital economy, complements LSO nicely. It’s a three-tiered conversational architecture in which:

A customer-facing top layer handles order capture, configuration and invoicing

A middle digital service lifecycle management layer offers dynamic service design, orchestration, assurance and delivery

A bottom layer handles resource management with physical and virtual systems.

The parallel concepts of LSO and DLSM both recognise the important role virtual functions will play in the development of operator networks and the delivery of dynamic, high-performance digital services to consumers.

Comptel is eager to be part of the conversation within MEF to help define how LSO standards evolve, and we believe our ongoing involvement with MEF will help us bring a higher level of expertise to conversations with our own customers around NFV-driven service orchestration.

Comptel will be showcasing and discussing the Digital Service Lifecycle Management including their FlowOne V solution for end-to-end hybrid network service orchestration at a number of events in the coming weeks.

The app has been a pop culture sensation since launching in the U.S., Australia, the U.K. and New Zealand. It’s the biggest mobile game in U.S. history, and enjoys 21 million daily users on average. The average mobile iOS user spends more time on the Pokémon GO than they do Facebook, Snapchat, Twitter and Instagram.

That level of engagement for a brand-new app is extraordinary. Recognising that fact, T-Mobile U.S. rolled out a compelling offer for its mobile subscribers as part of its “T-Mobile Tuesdays” campaign: free, unlimited data to play Pokémon GO for up to one year.

T-Mobile has been at the forefront of programs that make data available to subscribers for free. Its “Binge On” program allows customers to access more than 75 streaming video services without using their monthly 4G LTE data allotment.

Customers love streaming content and games, but they are reluctant to engage with certain activities because it’s perceived they might consume too much of their data allowance. Sponsored data programs let them engage with those services because the cost of data consumption is covered by an enterprise, such as the content provider.

Through agreements with streaming content providers or mobile app developers, operators remove the financial barriers that might have discouraged customers from accessing these data-hungry services. As an effective monetisation strategy, sponsored data endears you to your customers, establishes greater levels of satisfaction and loyalty, increases data consumption and creates long-term revenue-generation opportunities.

At this past TM Forum Live! in Nice, we demonstrated a business model for enterprise sponsored data through a Catalyst championed by Orange. Our initiative – which was awarded “Most Innovative Catalyst – Commercial in the Communications Industry” – used Comptel’s Intelligent Fast Data capabilities to create personalised data offerings for enterprise customers, allowing those enterprises to collect usage data and apply policy control.

It’s not just streaming content providers who can get involved. Operators could identify new avenues to revenue in the B2B market. A business could purchase a corporate data allowance, for example, that sponsors all data its employees use to access corporate services, like Office 365, via their personal mobile devices. That eliminates any potential hesitancy on the part of employees, who otherwise may not want to use up their personal data allowance for work purposes.

Whether for work or play, sponsored data programs could be a major opportunity for operators to drive more revenue opportunities from data services. As digital services take up a bigger share of smartphone usage compared to voice and mobile, these new avenues to revenue will be crucial for operator business growth.

Read more about Comptel’s Catalysts at TM Forum Live! 2016, which included partnerships with Orange, Telefonica, Salesforce and IBM. Keep up with the conversation around mobile monetisation at Nexterday.org, our reader community and online magazine.

Comptel participated in several partner showcases during last week’s TM Forum Live! 2016 in Nice, France, with one in particular reimagining the model of digital service delivery for the modern B2B and B2C customer.

As Comptel CTO Simon Osborne explained, Comptel partnered with IBM and Juniper Networks in an IBM Cloud-Based Networking architecture. The project introduces new strategies for leveraging software-defined networks (SDN) and network functions virtualisation. As a result, operators can efficiently automate and reconfigure parts of their network to enable automated, self-service digital service delivery. As part of the partnership, we’re contributing our Digital Service Lifecycle Management (DSLM) model, technology and expertise.

Digital Service Lifecycle Management (DSLM) architecture

In an earlier blog, I explained why this needs to happen. B2B and B2C customers today want personalisation, convenience and instant gratification in the purchasing process. Operators need to evolve their infrastructure to deliver better customer experiences to stay competitive, and network virtualisation gives operators the agility and flexibility they need to do so.

The key to introducing new capabilities gradually – since complete network overhauls aren’t practical for most operators – is to introduce “islands” of NFV capabilities into the network. On top of that, fresh approaches to managing the interconnection between physical and virtual resources will ensure operators can achieve this agility quickly, and at minimal cost.

In this post, I’ll explain just how you do that.

What is Digital Service Lifecycle Management

Comptel first introduced DSLM in our white paper – Digital Service Lifecycle Management: How CSPs Can Play a Successful Role in the Digital Economy. As Heavy Reading analyst Caroline Chappell wrote, operators today face competition from cloud-born companies like Google and Amazon, which have the infrastructure flexibility to spin up attractive new digital services much faster than the average operator.

Portraying the future role of operators as aggregators of digital services (from which the average consumer and business could buy whatever services they need to fill out their “personal digital ecosystems”), Chappell said network evolution is required to enable “on-demand personalised service creation.”

Digital Service Lifecycle Management (DSLM) layers

DSLM is how you evolve the network. It’s the middle portion of a three-tiered system that decides how virtual and physical network resources are managed to support service requests from front office systems.

How the Three-Tiered DSLM Model Works

This NFV-driven model requires three layers: one for resource management, one for digital service lifecycle management and one for business management.

The customer only ever sees the business management layer, which sits at the top and comprises the shopping environment, order configuration and payment tools. Customers configure and purchase services available through a digital catalogue, and automated ordering and billing capabilities ensure customer requests are quickly passed on for configuration and fulfillment.

The middle digital service lifecycle layer manages service composition through the service orchestration tool and the digital service catalogue. At this level, each new customer order is automatically checked for feasibility and availability, based on digital service definitions, service level agreements and inventory. That improves order quality and eliminates false service availability promises, which cuts down on customer dissatisfaction and the risk of order fallouts.

The resource management layer sits at the bottom and includes the infrastructure management tools and controllers that support physical and virtual network functions. When a customer inquiry for a new digital service arrives, this layer determines how best to deploy resources to fulfil that request.

With this NFV-driven model, operators can offer B2C and B2B customers alike a fast, accurate and automated, self-service buying experience. The digital catalogue can be scaled to include any new service, from your standard consumer or business IT and communications services, to network functionality, to IoT connectivity, to third-party SaaS solutions. That means operators can add to their capabilities as the digital economy grows and consumer demand evolves.

Where DSLM Fits in to IBM’s Cloud-Based Network

We brought our DSLM model to the IBM partnership, and it’s supported by FLOWONE, our service orchestration solution. Sitting in the middle between IBM’s Omni-channel Customer Engagement, and on top of a range of resource services and infrastructure tools that include Juniper’s NFV orchestration and infrastructure management solutions, it brings our vision for NFV-based fulfillment to reality.

The IBM Cloud-based Networking architecture was introduced recently at TM Forum’s Live! event but you can read more in the IBM Blog by Steven Teitzel, Telco Global Solution Exec – Network Transformation, IBM.

We invite you to visit Comptel at the Light Reading Big Communications Event in Austin 24-25th May to learn more about the Comptel model for dynamic digital service lifecycle management. Email [email protected] to schedule a meeting. Alternatively follow our updates and activity on Twitter (@shateley & @Comptelcorp) or via our LinkedIn feed.

Technology partnerships are crucial to innovation in telecommunications. At next week’s TM Forum Live! 2016, Comptel will demonstrate the outcome of several recent industry collaborations, all of which are designed to introduce new approaches to digital service delivery, customer engagement, data monetisation and networking.

Comptel is taking part in three distinct partner-driven initiatives, including two TM Forum Catalysts, individually led by Telefonica and Orange; and an IBM-led digital service architecture blueprint. The ultimate objective of each initiative is to open operators’ eyes to new possibilities for infrastructure management, service delivery and offer creation through NFV service orchestration and intelligent fast data management.

Our contributions vary by project. In two of the cases, we’re putting the digital service lifecycle management (DSLM) model that we introduced in Nexterday: Volume II, with our FLOWONE service orchestration technology, managing forward-looking approaches to service delivery. In the third project, we’re supplying expertise and technology in the creation of a new, progressive data monetisation strategy.

Forward-thinking approaches are crucial at a time when customers desire fast, intelligent, personalised offers. Operators are also keen to take advantage of dynamic, intelligent, highly automated and virtualised network environments to speed up innovation, time-to-market and to improve security.

Here’s what you can expect from each partnership, with guidance on how you can learn more and engage with Comptel and our partners at TM Forum Live! 2016.

IBM’s Target Architecture for Cloud-Based Networking

Comptel, IBM and Juniper Networks have developed a new approach to digital service delivery for B2B and B2C customers, incorporating an orchestration and fulfillment architecture that allows operators to better manage end-to-end service lifecycles in complex hybrid networks of virtualised and non-virtualised services.

The architecture is based on our DSLM proposition, which you can read more about in a recent blog from our CTO Simon Osborne. The end-game is a network that’s able to automatically and dynamically deploy network capabilities and agile services in a way that gives customers automated, self-service digital service purchasing and delivery.

To learn more, visit the IBM booth at TM Forum Live!

Open Source NFV Service Orchestration and Lifecycle Management Catalyst with Telefonica

Comptel is also participating in two TM Forum Catalysts, which are proof-of-concept initiatives that encourage technology partnerships in the name of industry innovation.

The first is the NFV Service Orchestration and Lifecycle Management based on Open Source MANO Catalyst – sponsored by Telefonica. Along with Indra and Etiya, the initiative centres on Open Source MANO (OSM), an ETSI project to develop an open source stack for NFV management and orchestration, demonstrated here within a hybrid network environment.

DSLM also plays a crucial role in this Catalyst, as does our FLOWONE V service orchestration solution. The aim is to test the OSM software stack in a practical context and analyse how it needs to evolve to be production-ready.

To learn more about this Catalyst, join Telefonica and Comptel for our theatre session on Tuesday, May 11, 14:30-14:50 at the Catalyst Theatre.

Orange’s Catalyst on a Mobile Sponsored Data Business Model

Finally, Comptel will take part in an Orange-championed Catalyst, “New Business Models with Mobile Sponsored Data,” which also includes partners Salesforce and CloudSense, plus Sigma Systems and DataMi. We’ve contributed our Intelligent Fast Data technology and capabilities to illustrate how enterprises can sponsor mobile customer data usage as a way to incentivise the use of enterprise digital services, increase data engagement, collect usage data and apply policy control.

To learn more about this Catalyst, attend our session titled “New Business Models with Mobile Sponsored Data” at the Catalyst Theatre on Wednesday, May 12, 13:40-14:00.

Comptel is proud to partner with each of these technology leaders in collaborative efforts to introduce new solutions to communications. Whether it’s by improving digital service delivery through new infrastructure models, further developing OSM, or enhancing customer engagement through the creation of new business models, we’re excited to pioneer digital transformation. We can’t wait to share our progress with attendees at TM Forum Live! 2016.

Visit TM Forum’s Catalyst Zone to see these Catalyst demonstrates in action. To arrange a meeting with Comptel at TM Forum Live! 2016, email [email protected]

It’s a really good time to be a shopper. The world’s top ecommerce marketplaces, like Amazon and eBay, make it easier and faster than ever for consumers to buy whatever they want on any device, at any time. Top brands are also striving to offer a better buying experience – you can go on Nike.com right now and fully customise and order your own pair of shoes without leaving your couch.

Personalisation. Convenience. Instant gratification. Customers want it all, and technology means top brands are able to deliver. As a result, we’re operating in a new digital economy, one that’s driven by personal choice and an experience-led approach.

So why are many operators still struggling to deliver a convenient, automated and engaging customer experience?

The digital service purchasing process needs to evolve, and since we first discussed this topic in last year’s Operation Nexterday, we’ve heard some great success stories from operators who are undergoing that transformation. But we’ve also heard from operators who need guidance devising and launching a new model for digital service delivery.

That’s why, at next week’s TM Forum Live!, we are launching a proposed architecture for digital service delivery in partnership with IBM and Juniper Networks. The IBM platform for Cloud Based Networking (CBN), intends to maximize the agility offered by network function virtualisation (NFV) and software-defined networks (SDN) to create a better model for service delivery in the digital age.

What NFV/SDN Can Do for Digital Service Delivery

As I wrote in a recent LinkedIn Pulse piece, the virtualisation of networks and services empowers operators to present customers with the right services at the right time. That’s because NFV and SDN offer the infrastructure agility and flexibility to rapidly create new digital services, including their operational aspects, at maximum speed and minimum cost. In other words, NFV and SDN allow operators to move fast enough to create a more immediate and satisfying digital customer experience.

Of course, given that the embrace of NFV technologies won’t happen overnight, this vision doesn’t require a dramatic shift to a fully virtualised network. Instead, operators will deploy NFV capabilities as “islands” within their infrastructure, leveraging existing physical resources and associated OSS/BSS platforms as part of a hybrid approach for some time to come.

The Comptel/IBM/Juniper initiative, which is built in accordance with the Comptel Digital Service Lifecycle Management (DLSM) model proposed in Nexterday: Volume II, takes this hybrid approach into account. Designed as a three-tiered architecture, DSLM relies on a central orchestration layer that manages requests from the top customer engagement and business management layers, and supports those requests with appropriate resources from the bottom virtual and physical resource layer.

Each layer works together to deliver automated order validation, self-service customer configuration and intelligent resource management for easy scalability.

Creating Reality from New Digital Service Possibilities

How would this all be exposed to the customer? Through a better digital buying experience.

Customers should now be able to self-configure and order a broader range of services from a digital catalogue, and the operator’s infrastructure would handle the automated creation and immediate fulfillment of those services.

In the enterprise world, businesses looking to add on a new IT or communications service will be able to abandon the legacy linear purchase process that’s plagued by lengthy requirements reviews, proposals and bids which lead to delays, fallouts or generic IT implementations. Instead, much of the enterprise sales process will be automated, helping operators improve experience and sales.

The model creates a foundation for operators to easily grow and deliver a wide range of new service capabilities. With NFV, operators are able to assume the role of digital service aggregators, setting up marketplaces for B2C and B2B buyers to purchase existing and emerging digital services. For enterprise customers, that might even mean buying the very virtual functions they need to provision their own networks.

Ultimately our partnership with IBM and Juniper aims to reveal the business potential of virtualised networks when applied to service delivery – and how it unlocks new possibilities for operator service growth.

We invite you to visit the IBM booth at TM Forum Live! in Nice, France, from 9-12 May to learn more about the IBM Cloud Based Networking initiative and our model for dynamic digital service delivery. Email [email protected] to schedule a meeting.

Posted: November 4th, 2015 | Author:Steve Hateley | Filed under:Events | Tags:NFV, service orchestration | Comments Off on NFV, Service Orchestration, and the New Speed of Service Delivery

In a recent blog, Light Reading reported that business considerations are driving operator interest in network functions virtualisation (NFV) just as strongly – and if not, more so – than technology drivers. In other words, more operators recognise that virtualised networks create new service opportunities and new means to generate revenue.

It all comes back to speed. With a more agile infrastructure, operators are empowered to move faster than ever in a number of areas, perhaps none more important than the speed at which they can deliver new revenue-generating services.

Digitalisation has introduced an entire industry of mobile and digital services that buyers love, from apps to over-the-top (OTT) content. At the same time, we’re living in the era of Generation Cloud, where customers expect instant gratification and a high degree of personalisation in their interactions with service providers.

And there are potentially many more services to deliver. Digital consumers across the board – from enterprises to individual consumers – are excited about the possibilities offered by emerging technology, such as the Internet of Things (IoT) and 5G connectivity.

As a result, whatever new services operators seek to offer in the near and distant future, it’s certain that NFV and SDN technologies will form the backbone of their service architecture. How will networks evolve to accommodate NFV, and what challenges will its implementation create in the management of existing operation support systems (OSS)?

Experts in the industry debate these questions every day, and this week Comptel will contribute our unique viewpoints during the Light Reading event “OSS in the Era of SDN and NFV: Evolution vs Revolution.” CTO Simon Osborne will host a keynote presentation on service orchestration and Strategic Product Manager Daniel Tyrode will join a panel discussion all about the role of service orchestration in programming the network for rapid service delivery.

These will also be key topics of discussion in Blueprint Alley at our inaugural Nexterday North event next week. If you haven’t already, there’s still time to register for that event and join the conversation around the future of service orchestration in light of the emergence of NFV and SDN.

Both events will address how the back office is influencing front office business decisions, and how operators can address the technical and operational challenges therein. Interestingly, the Light Reading blog mentioned one estimate that said 25 percent of telcos around the world are not fully on board with NFV, content to hang back and wait to see how the technology develops.

If they wait too long, those operators will find themselves at a disadvantage. Recent estimates from Appledore Research Group claim there are as many as 250 ongoing NFV trials and 25 early live deployments. A separate survey from Heavy Reading claims as many as 79 percent of operators expect to have a live NFV deployment by 2018.

Ultimately, many operators are ready to see what NFV can do for their bottom line. By finding technical solutions sooner rather than later, these telcos will more quickly be able to realise the benefits of faster service delivery.

Register today for a 2×2 Front Pass to Nexterday North (9-10 November) and receive full access to Slush, the massive startup conference that starts just two days later – running from 11-12 November.

The spotlight is shining brightly on network function virtualisation (NFV) as software vendors, hardware manufacturers and operators step up their investment in and engagement with this technology. As my colleague, Malla Poikela, wrote in a recent blog, ongoing NFV trials and projects were featured prominently at this year’s TM Forum Live. In the Storify post below, we track recent conversations and developments around this radical new NFV ecosystem. Take a look to see how the NFV discussion is constantly evolving.

And don’t forget to join us in November for our can’t-miss anti-seminar, Nexterday North, where the emerging NFV ecosystem will be one of many topics of discussion. Industry experts and innovators will be on hand to take a fresh look at telecoms through a new lens, and discussion will be framed around the three pillars of Thinking Ahead (looking at other industries to examine our collective blindspot), Thinking Again (re-examining industry learnings to challenge the status quo) and Thinking Beyond (learning from emerging startups who are disrupting the digital world).

Experts in the industry debate these questions every day, and this week Comptel will contribute our unique viewpoints during the Light Reading event “

Experts in the industry debate these questions every day, and this week Comptel will contribute our unique viewpoints during the Light Reading event “